Lognormal

Log-normal

|

Probability density function

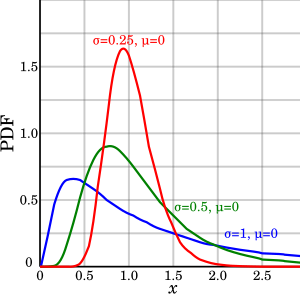

Some log-normal density functions with identical location parameter  but differing scale parameters but differing scale parameters

|

|

Cumulative distribution function

Cumulative distribution function of the log-normal distribution (with  ) )

|

| Notation |

|

| Parameters |

— location, — location,

— scale — scale

|

| Support |

|

| PDF |

|

| CDF |

![{\frac {1}{2}}+{\frac {1}{2}}\,\mathrm {erf} {\Big [}{\frac {\ln x-\mu }{{\sqrt {2}}\sigma }}{\Big ]}](https://wikimedia.org/api/rest_v1/media/math/render/svg/3cde9b1ecbbb13897c36b45898ebbd7cd2366ecc) |

| Mean |

|

| Median |

|

| Mode |

|

| Variance |

![{\displaystyle [\exp({\sigma ^{2}}\!\!)-1]*\exp({2\mu +\sigma ^{2}})}](https://wikimedia.org/api/rest_v1/media/math/render/svg/e283edefb1b3afc7e344a84d6a4d4edd51c20cd9) |

| Skewness |

|

| Ex. kurtosis |

|

| Entropy |

|

| MGF |

defined only for numbers with a non-positive real part, see text |

| CF |

representation  is asymptotically divergent but sufficient for numerical purposes is asymptotically divergent but sufficient for numerical purposes |

| Fisher information |

|

In probability theory, a log-normal (or lognormal) distribution is a continuous probability distribution of a random variable whose logarithm is normally distributed. Thus, if the random variable  is log-normally distributed, then

is log-normally distributed, then  has a normal distribution. Likewise, if

has a normal distribution. Likewise, if  has a normal distribution, then the exponential function of is

has a normal distribution, then the exponential function of is  has a log-normal distribution. A random variable which is log-normally distributed takes only positive real values. The distribution is occasionally referred to as the Galton distribution or Galton's distribution, after Francis Galton. The log-normal distribution also has been associated with other names, such as McAlister, Gibrat and Cobb–Douglas.

has a log-normal distribution. A random variable which is log-normally distributed takes only positive real values. The distribution is occasionally referred to as the Galton distribution or Galton's distribution, after Francis Galton. The log-normal distribution also has been associated with other names, such as McAlister, Gibrat and Cobb–Douglas.

...

Wikipedia